Blockchain Commercial Solutions Pt. 3 - Real World Assets

Centrifuge's Tinlake Case Study

July 9, 2021

In the previous piece (Blockchain Commercial Solutions Pt.2 - Insurance), we discussed how on-chain insurance might merge with traditional insurance offerings. Crypto-economic protocols enable new planes for data collection, claims execution, liquidity, and access to policyholders. More distributed markets for insurance will ultimately prevail, despite the perceived loss of control by insurers. More contracts will be unwritten, both by incumbents and bespoke insurers, and small entrepreneurs internationally will have access to insurance for the first time. The implicit through-line is: not only does insurance move on-chain, but that value of all kinds moves on-chain, to the extent that it makes sense to do so.

An insurance contract behaves differently than more liquid assets because it necessarily interacts with rocks and weather and crops—the real world. Sure equities, bonds, and options ultimately derive their value from activities pursued by real people in the real world. But the causal link between atoms and ticker tapes is looser. Hedges against real world uncertainty, be it agricultural futures or crop coverage contracts, are indissolubly linked to meat space. As readers will know by now, It is here, at the intersection of crypto and main street, that I find myself most intrigued and hopeful. To democratize insurance is to enable a basic building block for generating wealth—certainty that it won’t be wiped out overnight. Once the possibility of catastrophic risk has been shunted, entrepreneurs can more comfortably take risk on projects to grow their wealth.

The case for fractionalized, liquid financial securities like stocks, bonds, and options to move on-chain is fairly obvious. These securities should trade immediately, around the clock, and self-custodially. These types of assets are relatively easy to port on-chain. Whether these instruments are issued directly on chain (EIB Issues bonds on Ethereum) or are mirrored via synthetic assets (Synthetix), as long as an oracle mechanism properly updates prices, the value that these instruments represent will move from traditional exchanges and brokerages to blockchains.

Historically, highly liquid securities like stocks and bonds have been easier for investors to access and for institutions to issue. But the assets at the core of the economic engine, those of individuals and SMEs, have remained largely inaccessible. This is especially the case for hard assets like real estate and collectibles (art, cars, etc.), which tend to be indivisible and illiquid. They trade binarily, either in their entirety or not at all and usually among institutions or large, sophisticated buyers who wield clout, access, cheap capital, or all of the above. For the most part, an individual can not buy 10% of a house or the associated mortgage, half of a bottle of Suntory Hibiki 21, or a portion of the cash flows derived from short-term loans backed by trucking invoices. Protocols like Centrifuge and CurioInvest seek to change this. By bringing non-fungible Real World Assets (RWAs) on-chain, these protocols act as a conduit for capital to trickle to places that were previously inaccessible. When crypto can begin delivering solutions to normal people and businesses, it goes from a cypherpunk-studded fantasy speculation land to a liberator of capital. To begin mobilizing the universe of RWAs is to transport many millions of businesses and people into modern finance.

Porting RWAs on-chain: A Centrifuge Tinlake Case Study

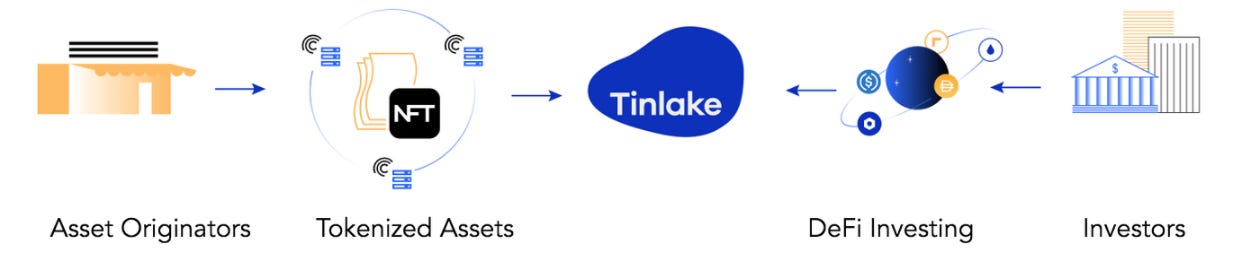

Centrifuge’s Tinlake has built a decentralized protocol that convenes asset originators and asset investors in one place. An asset originator is typically a business on the ground who is lending directly to borrowers. These can be real estate lenders, factoring companies, or anything in between. Assets like fix-and-flip mortgage notes, short-term trade financing notes, and music royalties are represented via NFTs and locked into Tinlake’s smart contracts. Investors can then freely invest in either of two risk tiers, getting direct exposure to cash flows occurring in the real world.

Fig. 11

With ten asset pools currently live, Centrifuge’s TVL (total value locked) has grown from $2MM as of January 2021 to ↝$26MM as of today. (Centrifuge). To give an example, one of the pools that is currently live is the “New Silver Pool 2”, which is composed of real estate bridge loans. These are short-term (12-24 months) loans meant to “bridge” a newly acquired property from unrenovated to renovated and sold. These fix-and-flip loans provide capital for both the acquisition and the improvements on the property. The New Silver Pool 2 currently contains 40 assets with an average duration of 12 months and an average interest rate of 6.80%. This revolving pool is dubbed “Pool 2”, as the first pool was static, a vestige of the protocol’s former structure.

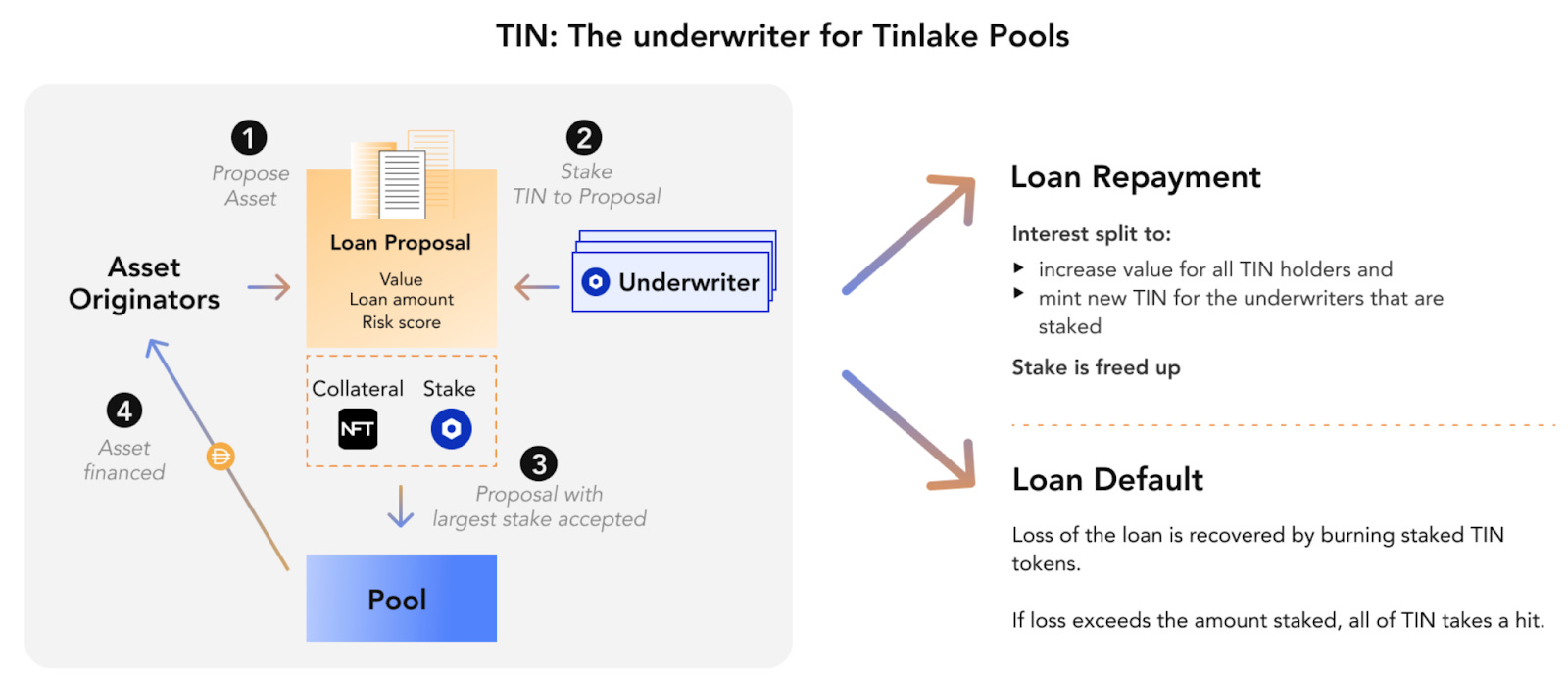

Let’s now consider how the protocol actually works. This examination will allow us to investigate how the protocol goes above and beyond traditional avenues for real world finance. First, asset originators propose assets to be included in pools. Then, underwriters examine the proposals for quality and credit worthiness. Underwriters might consider the proposed valuation of the underlying asset, the loan amount relative to that valuation (Loan-To-Value ratio), and the risk of the underlying credit. Beyond scrutinizing these basic assumptions, underwriters can apply any bespoke risk methodology they feel is compelling. Underwriters will then “vote” for certain vetted assets to be included in pools by staking value towards those assets. In this case, the value staked towards assets is TIN, one of the two fungible risk tokens native to the Tinlake ecosystem (more on this later). Other underwriters will review the active underwriters’ proposed loans and stake their TIN towards it if they agree that it is a good candidate for inclusion in the pool.

Once consensus on inclusion is reached, an NFT is minted that represents the economic interest of the asset. This NFT will include all of the relevant characteristics of the underlying asset: valuation, loan amount, risk score, duration, interest rate, etc. Importantly, embedded within the NFT is also an acknowledgement by both originators and underwriters that the information is accurate and that the associated transactions are legitimate. These acknowledgements are achieved by hashing, or digital signing. An SPV, or Special Purpose Vehicle, is created to act as the legal counter-party to both the investors and the asset originator. The NFT is then fed into a Tinlake smart contract and the risk tokens TIN and DROP are issued by the SPV to the investors who contributed DAI (a crypto-dollar) to the pool. Tinlake utilizes a revolving credit line2 (From MakerDAO) to nimbly deploy capital towards new assets entering the pools. Proceeds, denominated in DAI, a multi-collateral-backed stable coin, are remitted swiftly to the Asset Originators.

Entitlements to the cash flows from the assets in a given pool are represented via the fungible tokens TIN and DROP. DROP acts as a safer, senior tranche and TIN acts as a riskier, junior tranche (variable rate, first loss). When the underlying loan pays off, available cash flows first to DROP and then to TIN. Underwriters are compensated for their services via issuance of TIN. This underwriting fee is only paid when the loans pay off in full. This token design incentivises proper underwriting, as underwriters, through their TIN exposure, absorb first losses on the loans that they whitelist for inclusion. The tiered token structure accommodates both risk averse and risk-seeking investors.

Fig. 23

Now that we are familiar with the mechanics of the protocol, we’ll delve into how such a network might improve upon and eclipse the capacity of traditional finance (TradFi).

Liquidity: As discussed in the previous piece on decentralized insurance, many financial assets remain inaccessible to small investors. To the extent that Tinlake can bring a greater and more diverse array of investors into the fray, it can support new planes of liquidity. Anybody with a cryptocurrency wallet, who is whitelisted/KYC’d, can invest in these assets. The RWAs that Tinlake is onboarding provide investors with yield that is relatively safe and largely uncorrelated with broader, volatile crypto markets. A larger supply of investment drives competition which drives cheaper financing for asset originators. Tinlake is not yet cheaper than incumbent options, but as competition for investment rises, it will become comparable and even more affordable.

Further, in my view, Tinlake/CFG are taking a hack at standardizing the process for origination of and investment in assets of an idiosyncratic nature. Take trade finance. The originating and underwriting of these loans is a labor intensive process because the credit risk is quite heterogeneous. The variance of exposure is greater: some borrowers have higher fraud risk, some borrowers are more or less solvent, some are requesting a shorter duration loan etc. It is very difficult to construct a traditional securitization market for these assets because they are all so different. Further, the loan amounts tend to be smaller than those in, say, mortgage pools. So there is less institutional appetite to buy into pools. So originators of trade notes typically hold much of the exposure to their borrowers on the books. To offset some risk, they will invite deeply vetted institutions to “participate” in some exposure. Instead, Tinlake allows originators to test a market composed of individuals who underwrite the proposed assets actively. These originators receive quick feedback as to whether their assets are of sufficient quality for inclusion. As originators adapt to the preferences of the pools, they will be able to more predictably access capital for assets that were previously difficult or expensive to market. Originators who can more consistently offset risk and receive proceeds can then go and originate more loans that can be sold into pools. A virtuous cycle.

Ease: One of the more general benefits of using blockchains is the capacity to transfer value reliably, 24/7, and in minutes. On Tinlake, originators will receive funds more quickly than in traditional avenues for financing. Tinlake draws on a revolving credit line, or a warehouse line, to remit funds immediately to originators. As soon as the NFT representing the digital asset is ingested by the Tinlake smart contracts, funds denominated in DAI are transferred to the originator’s wallet. No business days, no delays. Self-custodially.

Underwriting: As is the ethos in broader crypto, Tinlake converges investors and originators, obviating the traditional middleman. In the traditional securitization mode, for example, banks pooling assets (say commercial mortgage backed securities) approach rating agencies for credit risk ratings. These credit rating agencies are paid by the bank/issuer and are thus not incentivized to grade the risk optimistically. We saw some of the repercussions of the issuer-pays model in 2008. In a non-securitization model, asset originators approach one or a few smaller banks who are intimate with the asset class. Because A) the banks are the ultimate investors in the debt and B) because competition for the business tends to be low, the cost of capital tends to be uncompetitive, which is clearly not in the best interest of those originating assets.

The Tinlake protocol is structured such that many individuals can underwrite assets proposed for inclusion in debt pools. This is a different model than in traditional finance, where a single team at a bank/intermediary is responsible for vetting assets. Currently, Tinlake does not provide all that much incremental benefit to large businesses and asset originators who can already access cheap credit. But for SMEs the journey to financing is more complicated. They are unable to access cheap credit lines from banks and thus interface with alternative lenders. These include regional banks, factors, merchant cash advancers, hard money lenders, bridge lenders, credit unions, etc.

Tinlake’s underwriting process for assets is distributed across many contributors. This structure enables a broader set of underwriting methodologies and potentially more robust underwriting across many different industries. Instead of approaching individual venues for financing assets, SMEs can simply test the underwriting pool for interest. Because Tinlake is an open protocol, a variety of underwriters with varied expertise can evaluate a bevy of loan types with different characteristics. The diversity of assets being proposed broadens the breadth of underwriters entering the system, and vice versa.

Critically, Tinlake has shrewdly structured its tokenomics and token design to align the interests of underwriters and investors directly. Because underwriters receive compensation for their services in TIN, the junior and more risky pool token, they have direct skin in the game. In fact, when a poorly underwritten loan defaults, it is the underwriters who absorb much of the loss. Further, only those underwriters who are actively involved in proposing loans for inclusion and/or delegating towards other underwriters’ propositions are rewarded with TIN issuance. Passive holders/speculators will thus lose purchasing power, which incentivizes direct participation in the protocol.

To summarize, Tinlake has identified the deep flaws in traditional RWA financing and leverages the range of crypto-economic incentives to make investing in and originating RWAs easier, simpler, and more robust. Through its P2P venue, Tinlake strives to enable anyone to become an originator, an underwriter, or an investor. Along with strong embedded incentives, these three groups respectively keep the opportunism of the other groups in check. Through integrations with money market and borrow/lend protocols, Tinlake is able to nimbly deploy capital to deserving originators. As the TVL grows, Tinlake will begin building out larger, more diverse pools collateralized by like-kind assets across many originators. We can envision solar panel financing, unsecured loans to content creators, student loans for trade school, and equipment financing entering the ecosystem. This multi-collateral structure will make pools even more anti-fragile and draw in a broader set of underwriters and investors. The journey to bring real world assets on-chain is by no means easy. But Centrifuge, virtually a lone wolf within the sector4, is making laudable progress in erecting the bridge from main street to crypto.

Through-Line: Blockchains Solving Real Problems for Real People and Businesses

Both CurioInvest and Centrifuge look to attack a similar problem: How do we make it easy for asset owners and asset investors to interact transparently and simply? By using a blockchain these protocols leverage an immutable ledger for owners and investors to refer to. Further, both tap into the reliability and tamper-proof attributes of smart contracts: the conditions innate to the smart contract are visible and value is transferred automatically. By making non-fungible and historically indivisible assets more fungible via tokenization, these protocols bring real liquidity to wealth-generating assets.

As an observer, I see the burgeoning movement to bring RWAs on-chain as a harbinger for the financialization of nearly everything. If unique assets (value) can be represented comprehensively on a blockchain, then fungible tokens can be issued and freely traded. I do not at all mean to ignore or downplay the importance of off-chain systems informing and bolstering on-chain financialization. Robust husbandry, legal, and liquidation processes must be in place to give agents confidence around the feasibility of porting meat space assets into cyberspace. These protocols will evolve with victories and crises along the way. As individuals take the plunge into asset financing on a blockchain, it is difficult to imagine reversion back to traditional venues. Adoption will happen gradually and then all at once.