2022: The Great Dispersion

Stocks <> Bitcoin, Bitcoin <> Crypto

Little Fires Nowhere

2.2.2022

Humans almost always overestimate their capacity to control natural systems well. We construct simple narratives to explain complex phenomena. This reduction leads us to meddle with such systems to great peril.

For many years, the protocol for fighting forest fires prescribed eliminating any small blaze. For a time, this zero tolerance strategy seemed to work quite well. The fighters’ mandate was to protect wildlife. Forest fires killed wildlife, after all.

We misunderstood. Small fires are a feature, not a bug. By eliminating the old and decaying, resources are re-channeled into the young and healthy. Through creative destruction, the system grows stronger. Contrarily, each time we suppress a small blaze, we add more fuel to a fire of the future. A great fire that we may or may not be able to control.

The Federal Reserve: S&P Fire Department

The US Treasury and the Fed have been snuffing out fires since the great depression. More recently, they’ve extinguished the GFC and COVID blazes. Instead of trucks, planes, and brigades, the duo wield quantitative easing, fiscal spending, and a benchmark rate. But ultimately the tactics are identical to those of the fire-fighters: dump liquidity into the system.

At a high level, when the Fed adds liquidity to the system, lower interest rates increase access to money. Easier money expands economic and financial activity. Interest rates are also used to discount future cash flows on risk assets like stocks and bonds. When rates are low, the present value of future cash flows rises. So lower rates should, all else equal, push higher the prices of outstanding fixed rate bonds and equities.

When the Fed removes liquidity from the system (or threatens to), either by selling bonds or by increasing interest rates, money becomes harder to access. This leads to a decrease in economic activity and an increase in the rate used to discount risk assets. The future cash flows “attached” to stocks and crypto are now less attractive than safer, short-term alternatives. So higher rates, all else equal, push lower the prices of risk assets with future cash flows (fixed rate bonds, equities).

As per recent FOMC commentary on how it intends to address inflation, the Fed's bond buying (quantitative easing) program will allegedly slow to a halt by March. Markets have priced in four rate hikes in 2022. Assets have sold off materially over the past month:

NASDAQ: -13.7%

S&P 500: -8%

Bitcoin: -30.5%

Ether: -39.3%

Markets are complex and prices have many lords. But the Fed seems to be the Emperor of the era. Depending on its resolve, an inferno may be left to blaze through the asset forest. It actually matters less *if* the Fed has the balls to pull liquidity from the system. What matters is that the threat hasn’t been so credible for a long time. 7% CPI and 3.9% employment form a ripe backdrop for follow-through.

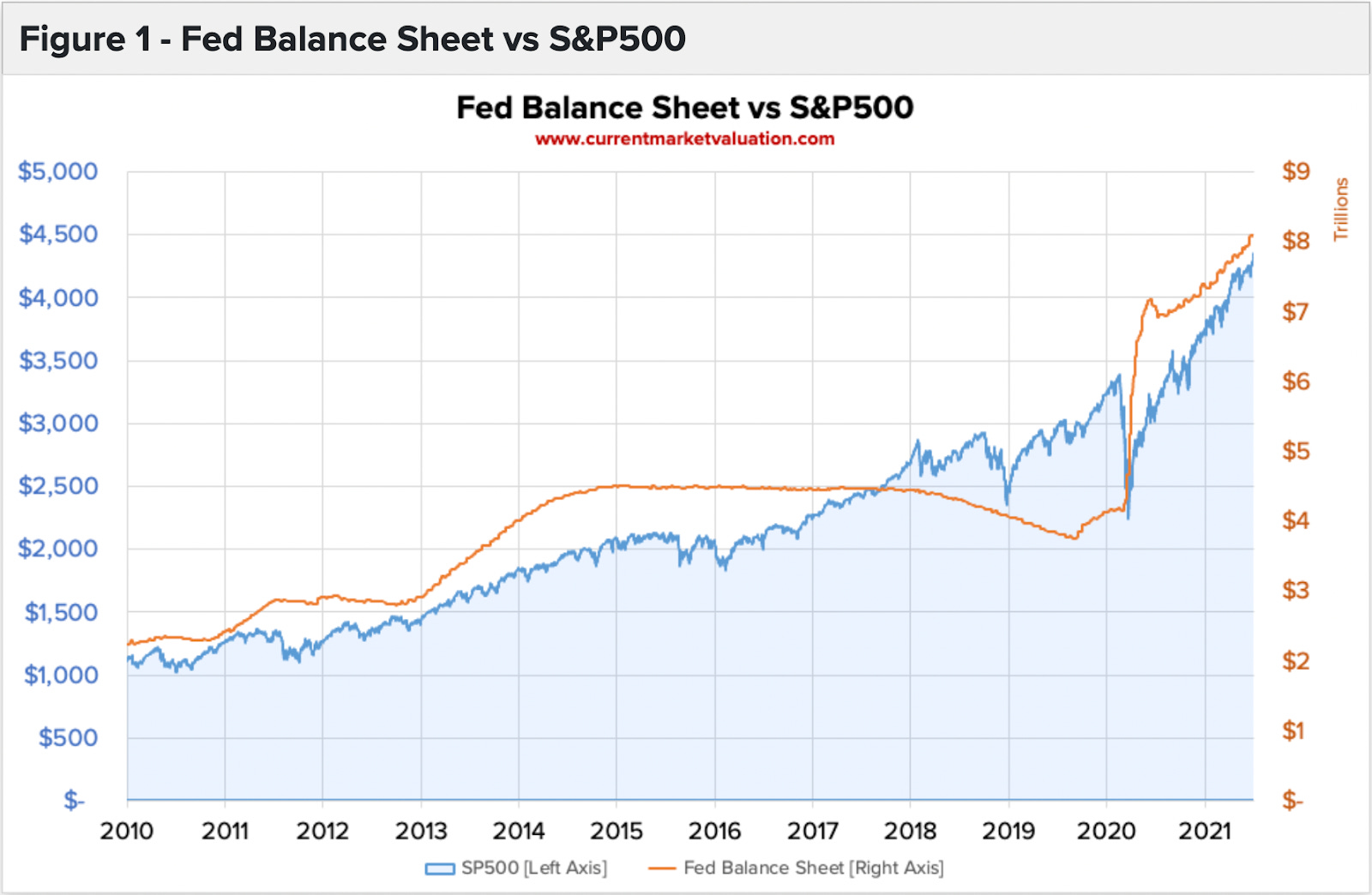

For twelve years, assets have generally moved up and to the right—the forest has grown in uniformity, coddled by the constant drip of liquidity (See Figure1). The Fed doves reigned supreme and the threat of the hawks remained muted. Now, the investor is left in a chamber of reckoning: if the Fed’s hoses really run dry, which of these assets do I actually believe in?

Of course the more I learn about crypto, the more I realize I don’t understand. But I know enough to be dangerous. And I think we are at an inflection point in the life-cycle of the industry. I believe we are entering an era of decreasing correlation and increasing dispersion.

The Great Dispersion

PART 1: The Decoupling of Crypto and Stocks

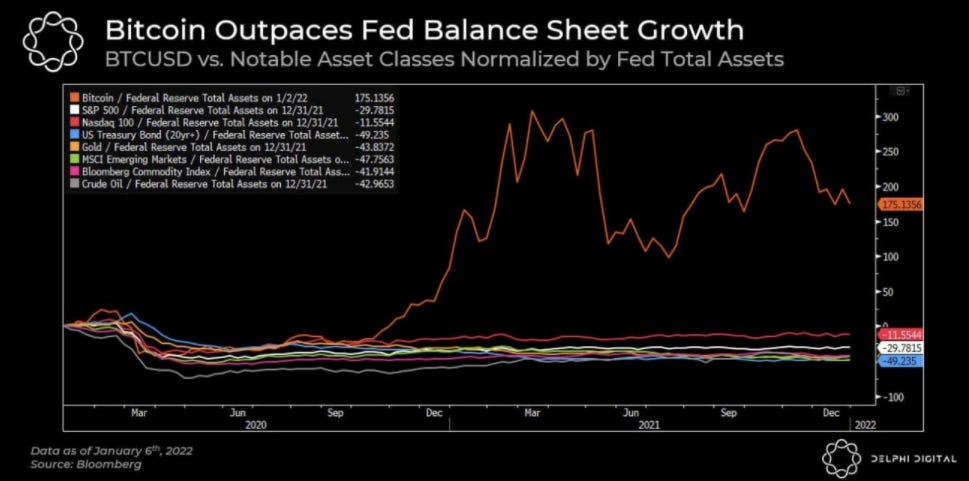

To the extent that assets are driven by the same things, they should move together. And vice versa. The fundamental forces that drive stocks and crypto are increasingly diverging. Stocks are more wholly reliant on a single source of energy, artificial liquidity, than are tokens. Crypto can and will draw on a number of energy sources. Over the medium term, the removal of liquidity will only pull crypto down as far as those countervailing energy sources allow.

*Bitcoin: Orange line at the top, Non-crypto risk assets: collection of flat lines. Sorry for the fuzzy graphic. Source: Bloomberg

Crypto is the internet of value. By this token, its root network permeates cyberspace in a way that other asset classes simply do not. Fueling digital culture and society, crypto will undergird the next leg of economic expansion: the gamification of finance and the financialization of gaming. It has mainstreamed far more than most understand or are willing to admit: subcultures, countries, companies, and individuals will all start playing the new game.

Subcultures

People derive meaning from culture. Stocks respond to culture insofar as the underlying companies are able to monetize culture. But for the most part, stocks and culture do not have a reflexive, nor symbiotic relationship. Crypto not only responds to, but participates in and gives rise to culture.

DAOs, to crypto what corporations are to stocks, enable subcultures to mobilize, grow awareness, and raise and deploy a treasury in the real world. ConstitutionDAO, LinksDAO, KrauseHouseDAO, and CityDAO were recently profiled in the New Yorker. Crypto exchanges Crypto.com and FTX have forged a bridge to mainstream sports by spending hundreds of millions on stadium naming rights. TopShots, gameplay clips licensed by the NBA, boasts 644,00 holders and $884MM of volume since launch. Sotheby’s and Christie’s are selling NFTs while Steph Curry and Jimmy Fallon use Bored Apes, an NFT project on Ethereum, as their Twitter profile pictures. The takeaway here is not all that cerebral but may nevertheless be interesting to readers: crypto is a completely different animal. It is dynamic, complicated, messy, and yet accessible. NFTs and (fungible) tokens are inextricably wrapped up in cyberspace culture. Tokens are not stocks and will only maintain so much connection to their prices.

Previously the Staples center, crypto.com paid $700MM for the naming rights to the Lakers/Clippers home court.

Countries

The game theory behind nation state treasury activity is complex. But we can start with a few basic assumptions to inform how we might think about crypto’s role and how it diverges from that of stocks:

1. Countries want to maintain powerful fiscal and monetary tools to achieve economic goals. Within this toolkit are central banks (FX reserves) and sovereign wealth funds, which address short term and long term goals, respectively.

2. Countries want to maintain economic autonomy and reduce reliance on foreign nations

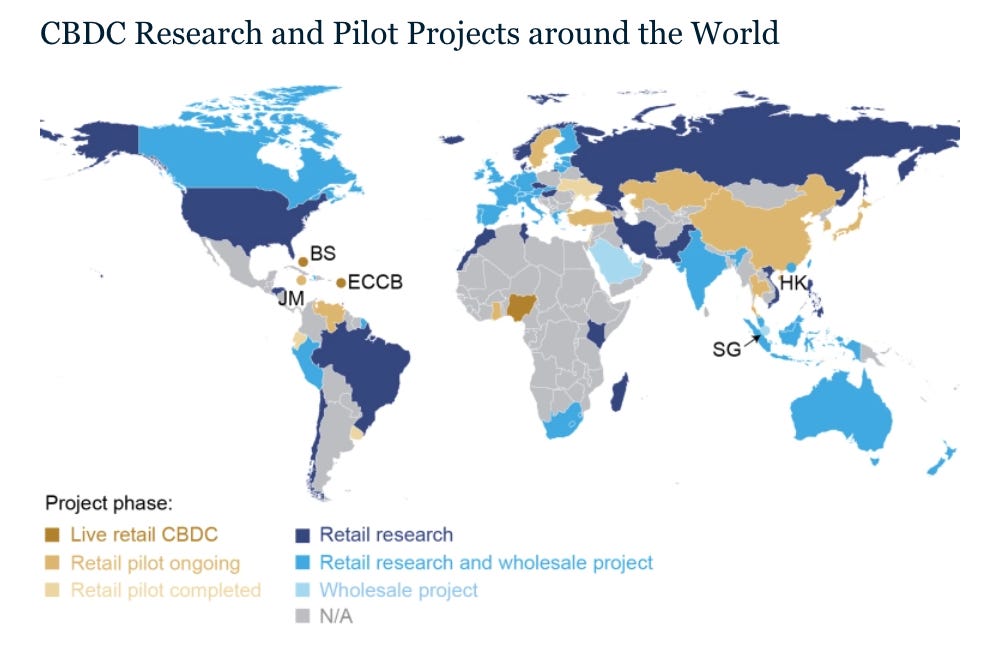

Foreign exchange reserves are a key primitive of currency management. Central banks will buy or sell FX reserves to strengthen or weaken the domestic currency as immediate economic conditions require. Within crypto, bitcoin is the most likely asset to land in FX reserves. It might add diversity to the holdings and potentially replace gold, which is expensive to liquidate, transport, and defend. A related but less important consideration is how central banks will choose to deploy central bank digital currencies (CBDC). The Nigerian government might choose to integrate with Algorand, a Layer 1 blockchain, this would serve as a natural bridge for millions of young, digitally native users into the ecosystem.

Source: New York Fed, Note: Nigeria is running a live CBDC beta as of 09/2021

Sovereign Wealth Funds (SWFs) will weigh the benefits of crypto vis a vis long-run strategic goals. These vehicles serve to generate long-duration, predictable yields by diversifying a nation’s revenue away from volatile natural resources. An effective SWF will help hedge its sovereign against the resource curse and maintain long-run purchasing power. Examples are Norges Bank Investment Management (NBIM) and the Abu Dhabi Investment Authority (ADIA).

SWFs hold mainly fixed income, real estate, and equities. Bonds are becoming increasingly inert as interest rates approach zero. With any inflation, real yields are thus negative. Real Estate is operationally intensive and subject to local geopolitics. Private and public equity is near all time highs and, as recent events suggest, vulnerable to Fed policy and inflation. More importantly, SWFs are effectively maxed out on growth stocks. NBIM owns 1% of each FAANG stock other than Netflix. As generational stewards of capital, SWF managers must recognize when paradigm shifts like the internet or mobile waves are afoot. These groups will not miss crypto.

I agree with Michael Saylor’s characterization of bitcoin game theory. Generational money managers (e.g. SWFs, family offices, billionaires) with long time horizons will recognize the asymmetric upside of modest bitcoin exposure. Bitcoin serves as impenetrable, digital property that tends to trend higher over the long-term. They’ll also recognize that other managers recognize what they’re recognizing. Seeking to front-run the meta-game, allocators will spring into action, lest they be forced to buy on the back of their peers, appearing luddite and slow. A few managers (Saylor, Elon, Paul Tudor Jones) turns into a party (Mubadala, OakTree, ADIA, SoftBank) and then everyone is off to the races. The allure of reducing reliance on fossil fuels and appearing futuristic will land particularly well among gulf states.

Economic autonomy is a basic condition for sovereignty, control, and national pride. Most countries are tethered to the US in one way or another. Because of the liquidity, scale, and power of dollars, countries are effectively forced to hold them on reserve. A country like Russia might pare its reliance on the dollar by replacing USD reserves with Bitcoin. Sanctioned countries, like Iran, at risk of being cut off from SWIFT and dollars might seek a similar solution. Further, fully dollarized countries like El Salvador might seek to extricate themselves from dollar policy by making crypto legal tender. Easing tax treatment of crypto might bring about wealthy and skilled in-migration. El Salvador will be the first of many countries to add crypto to its economic armory. One is not sufficient for social proof. But when the next sovereign follows, the dominoes will fall.

Source: IMF

Excepting Sovereign Wealth Funds and CBDC experiments, countries will initially interact with crypto primarily via Bitcoin. Bitcoin is lindy and could make the most meaningful impact on economic, political, and social goals. I see the pursuit of Bitcoin akin to the Age of Exploration. It is highly risky to be the first, but nations certainly don’t want to be last.

Companies

Web2 and traditional finance, the interest groups with the most to lose by legitimizing crypto, have voted it in with their feet. Facebook has changed its name to Meta and Square has changed its name to Block. Twitter will allow users to verify NFTs while Nike has acquired digital sneaker brand RTFKT Studios to position itself squarely in the Metaverse. Youtube is simultaneously scrambling to roll-out an NFT strategy as it loses its Head of Gaming to Ethereum side-chain project Polygon. Blackrock has filed for a crypto ETF while Lloyd Blankfein recognizes that “crypto is happening” and Goldman claims that the Metaverse is an “$8 Trillion opportunity. Visa has purchased a CryptoPunk. Paypal, CashApp, and Venmo have all rolled out crypto integrations. I could keep going but let’s not beat a dead horse into oblivion. The point is: stocks and crypto are no longer competing directly. Tech, finance, and their respective securities will lend their energy to crypto as it engulfs all digital value.

Individuals

In the West, the socio-economic zeitgeist will help feed a divergence between traditional assets and crypto. Young westerners are experiencing stagnating wages and increasing costs of living. Wealth inequality grows as asset owners gain purchasing power and young savers lose it. The younger generation cannot afford to store their wealth in traditional assets like real estate and stocks at all time highs. And so they’ll refuse to play the ponzi game that their parents did.

Instead, they’ll play their own game. One that involves blockchains, tokens, and DAOs. One that the older generation has trouble understanding. One that they can be early to. Only 3.9% of the world and 8.3% of America own crypto. We can expect the imminent growth in these figures to skew disproportionately towards millennials and Gen Z. We ought not to underestimate the magnitude of this cultural force—one propelled by pride.

Outside of the Anglosphere, crypto’s appeal is driven more so by need than desire. Permission-less financial services offer an escape hatch from volatile currencies and totalitarian overreach. The surging international demand for basic banking, payments, and investment options will provide a consistent source of uncorrelated energy to crypto. As an American, I often forget that international savers don’t have a luxurious matrix of choices: real estate (with property rights) or high-yield bonds, money market funds or tech stocks. Nobody in India, Nigeria, or Turkey is choosing between crypto and stocks. Crypto is the only game in town.

Pivoting to employment trends, traditional finance and Web2 are at the very beginning of a brain drain to Web3. YouTube losing Ryan Watts to Polygon is no outlier. Apple ponied up $180K bonuses to disincentivize top engineers from moving over to Meta, a clear indicator that people want to work on Web3. Because “the industry has matured and now offers comparable salaries with more potential for significant equity in the firm, and therefore, higher potential upside”, crypto is pulling talent from TradFi as well.

In summary: Young Westerners want to be early and own assets. Those in emerging markets need access to tamper-proof financial services. Talented engineers, investors, and bankers want to work on more interesting problems, have more flexibility, and earn more. Human motivation does not change, but the technological vectors that transport individuals to their desired end states do. In 2022, at the level of the global individual, few vectors carry as much upside as crypto does.

Conclusion: Decoupling of Stocks and Crypto

For most of the last decade, crypto was sort of a riskier extension of other, more well-known asset classes. It played second or third fiddle because it couldn’t boast any organic activity to speak of. This changed in 2020 with DeFi summer when it became clear that speculation finally had a counterpart—innovation.

At $2 Trillion dollars, crypto is 5% the size of US equities (roughly the size of Google). As the GDP of the industry grows, it becomes increasingly autonomous, shifting from purely an importer of speculative capital to an exporter of technological productivity. Because crypto will continue to innovate faster than other industries, its tokens will decouple from their equity.

PART 2: The Decoupling of Bitcoin and Crypto

Bitcoin is crypto, but crypto is not bitcoin. Borne of the great financial crisis, bitcoin is a unique beast—a direct antidote to excessive firefighting. As a contra-asset, it draws much of its energy directly from the excesses of the current fiscal and monetary regimes. For these reasons, Bitcoin is fundamentally a macro asset.

Since inception BTC has served, to varying degrees, as the mothership of crypto markets. When it moved, it pulled everything along with it. I think this relationship can be explained by a few factors:

Wealth Transfer: Bitcoin was first. Many grew wealthy through investing early. As BTC rose, these holders felt wealthier. This emboldened them to move out on the risk curve.

Canary in the Coal Mine: For many years, there was an existential angst that crypto was a temporary phenomena. When BTC sold off, it would confirm that angst and accelerate selling of lower conviction long-tail assets.

Relative Ecosystem Weakness: Prior to 2018, there was very little developer activity on Ethereum, never mind on other Layer 1 ecosystems. Without any innate stickiness to ecosystems outside Bitcoin, it took only small moves in BTC to prod speculators to dump everything else.

While it will continue to serve some role as a bellwether for capital entering the space, I am betting that BTC’s gravitational pull will decrease over the course of 2022/2023. Smart money will begin to recognize how heterogenous innovation in the space is. As the space fans out and fundamentals diverge, covariance between bitcoin and broader crypto will increase.

Bitcoin and Ethereum: Fundamentally Different Bets

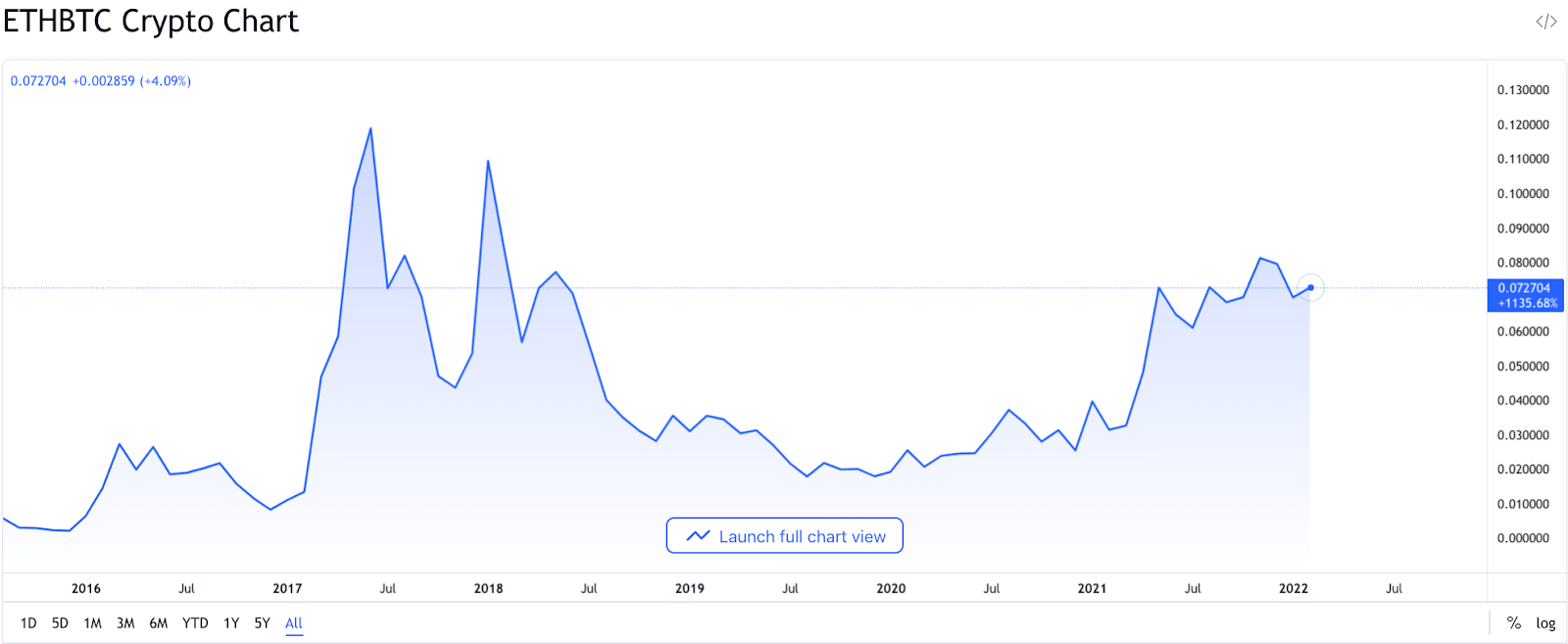

Bitcoin represents a monetary schelling point for agents seeking protection. While BTC is a bet on societal regression, Ether is a bet on societal progression. A gold bug might hold BTC while a technological optimist is more likely to hold Ether. With some exceptions (like Lightning Network and Stacks), Bitcoin does not support the development of applications. For many years, despite its capacity to, neither did Ethereum. That has since changed—Ethereum now supports a thriving digital economy. The two blue-chips represent different value propositions and draw on different sources of demand. As such, I expect their long-run price behavior to diverge even further: Ether’s market cap relative to Bitcoin is approaching levels not seen since June 2018.

Source: TradingView

Bitcoin Dominance Falls as Ethereum Strengthens

Bitcoin dominance (BTC.D), or the % of total crypto market cap commanded by BTC, flirted with all-time lows of ~39% recently. We can think of this level as a psychological threshold, or resistance line, for BTC as a bellwether. Meanwhile, Ethereum dominance (ETH.D) is currently ~20%, approaching its all-time high of 23.8% in January of 2018. Ethereum hosts 3x the developer activity it did in 2018. As time passes, other Layer 1 ecosystems will mature similarly and accrue value. Just as Ether will slowly divorce from BTC, so will other tokens.

Source: TradingView

As Crypto Diversifies, Bitcoin Loses Gravity

The Ethereum/Bitcoin duopoly on attention, developers, and capital has long since disappeared. For the most part, my readers know that Bitcoin and Ethereum entail very different propositions. They may not know that the diversity inherent to Ethereum is a fractal of broader crypto.

Relative to when I started studying it in late 2019, crypto has exploded in activity. It is now impossible for one individual to be completely caught up on the industry. Crypto is now home to over 50 smart contract platforms, each with a different ecosystem of decentralized applications (dapps) built on top. Some dapps focus on bringing trustless financial services to underserved countries. Others seek to bootstrap a market-based incentive system for reversing climate change. Others are enabling music NFTs, or games, or social networks.

Holders of Cosmos (ATOM), Decentraland (MANA), Aragon (ANT) invest for drastically different reasons. Cosmos is a bet on a world of interconnected, but sovereign blockchains. This is in many ways a bet against Ethereum. Decentraland is a bet on a community-owned alternative to Meta’s rather unimaginative and dystopic vision of the metaverse. Aragon is a “picks and shovels” bet on the proliferation of decentralized autonomous organizations (DAOs) as a primitive for human coordination. These three protocols ffer a microscopic sample of the innovation occurring across the space.

At this stage, the ambit of crypto protocols is far too broad for the entirety of crypto to move monolithically. As nation states, companies, and billionaires accumulate bitcoin, its value will increase but its role as a bellwether for broader crypto will not.

Disclaimer: Lupine Capital I, LP or TJ Ragsdale may own some of the tokens mentioned in this piece. This piece is intended to be educational in nature and is not financial ad